Get Expert Financing

- Matched with investor-friendly lenders

- Fast pre-approvals-no W2s required

- Financing options fro rentals, BRRRR, STRs

- Scale your portfolio with confidence

While most armed forces members are aware of the VA Loan program, they may not be aware of some of the important details, such as the VA Loan Residual Income Charts and why they matter.

Unlike traditional lending criteria that primarily focus on credit scores and debt-to-income (DTI) ratios, VA loans introduce a distinctive requirement: residual income.

This critical financial indicator ensures that borrowers have sufficient funds each month after covering major expenses to comfortably manage their living costs.

This article seeks to help you understand the importance of the VA loan residual income charts in the VA loan approval process.

Residual income—within the context of VA loans—refers to the money a borrower has left each month after paying off major debts and obligations, including:

The Department of Veterans Affairs uses this metric as a key indicator of loan eligibility and financial stability.

By assessing residual income, the VA can better gauge a borrower’s ability to handle unforeseen financial burdens, thereby reducing the risk of default.

The VA’s emphasis on residual income requirements serves a dual purpose:

This focus on residual income, rather than solely on DTI ratios, acknowledges that a holistic view of a borrower’s financial health is essential.

DTI ratios provide a snapshot of debt versus income but fail to account for veterans’ actual living expenses.

Residual income fills this gap, offering a more accurate reflection of financial resilience.

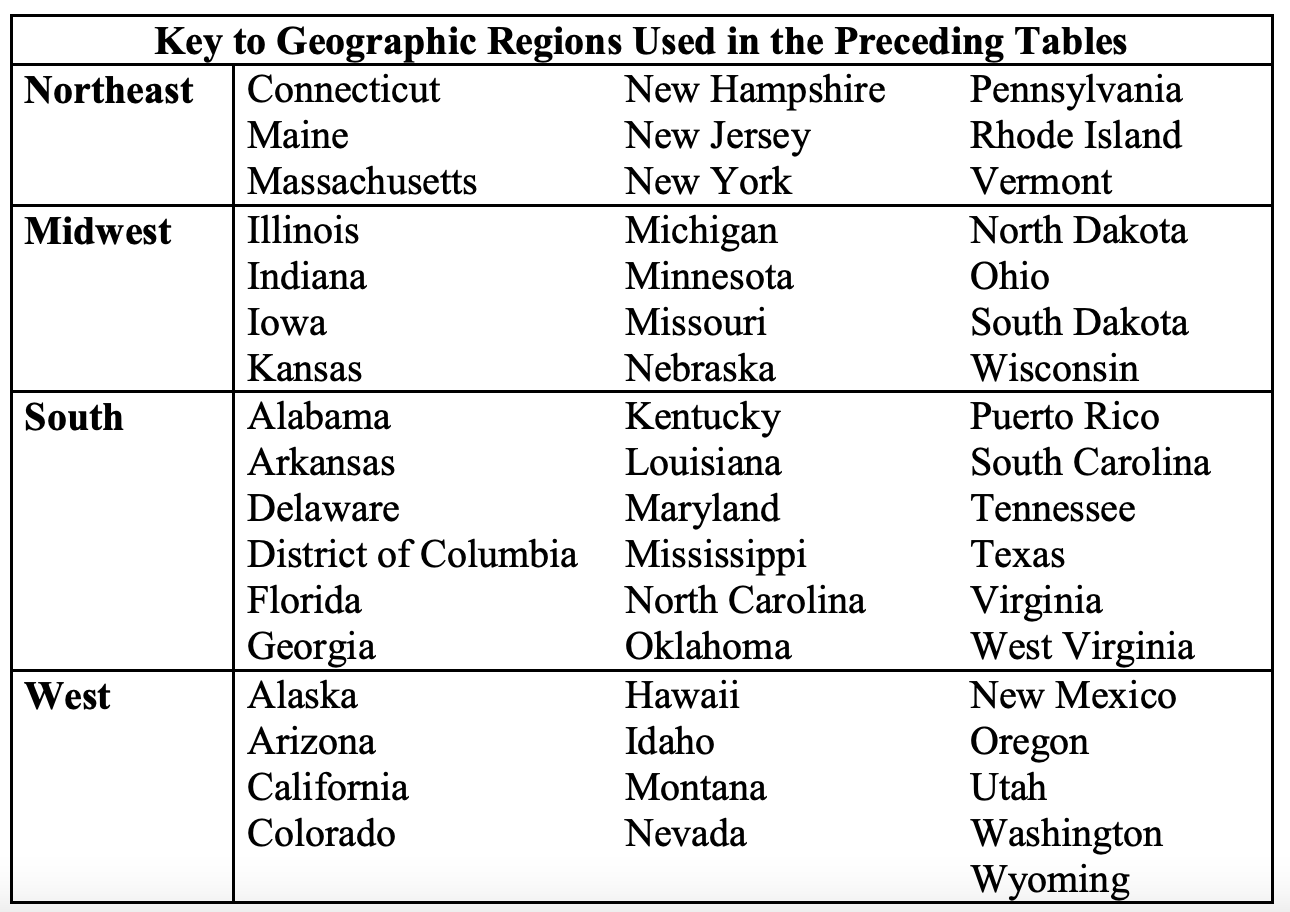

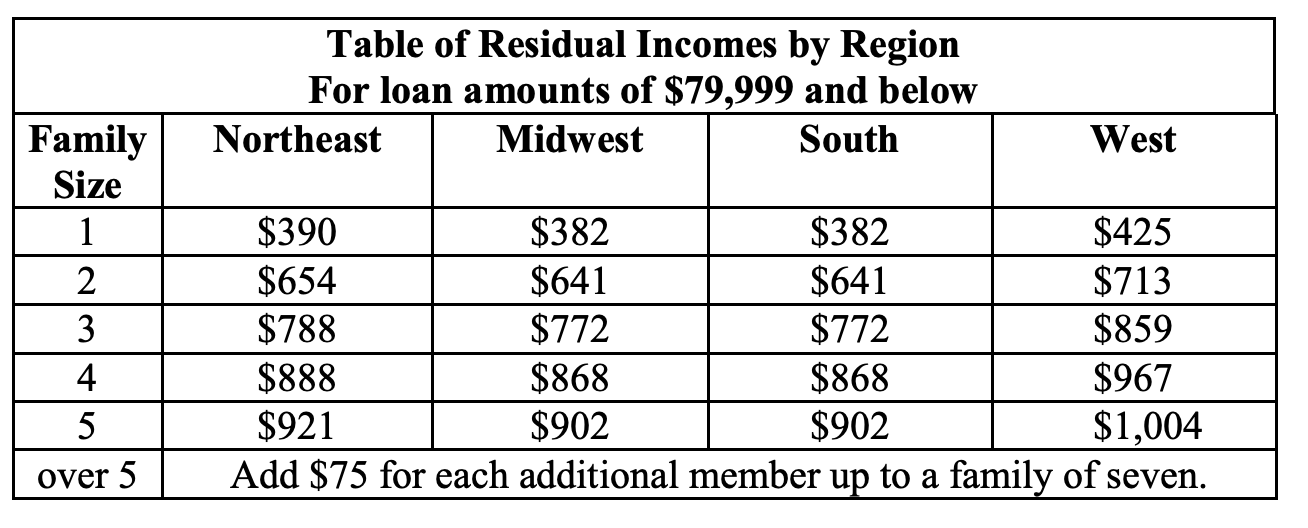

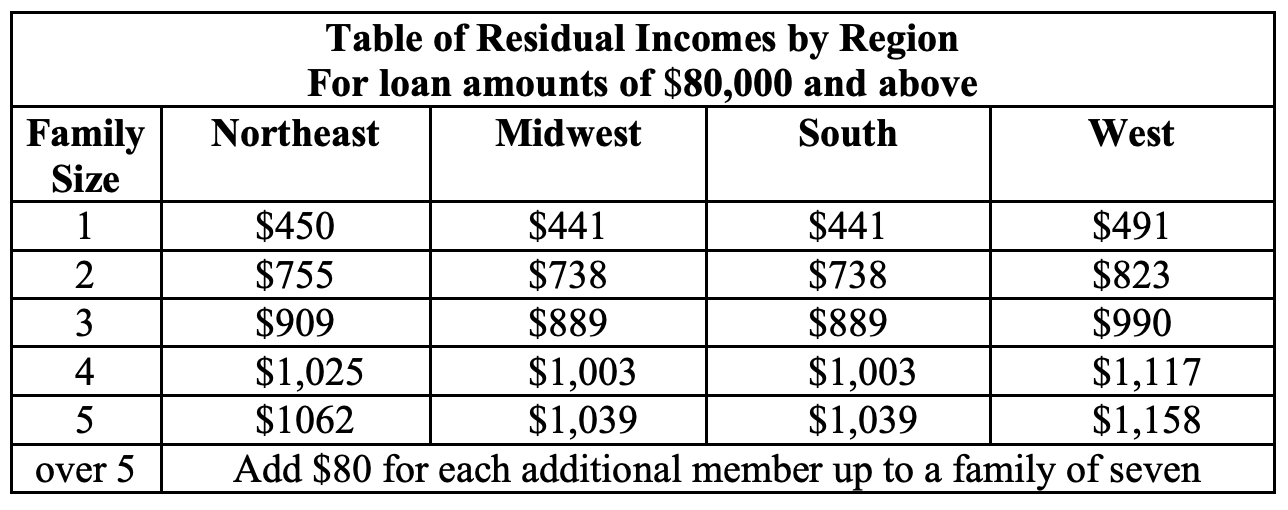

Navigating the VA Loan Residual Income Charts is simpler than it may first appear. These charts are structured around two main factors: the borrower’s family size and geographic location. Here’s a step-by-step guide to interpreting these charts:

The United States is divided into several regions, each with its residual income requirements.

Here is the chart in question:

Residual income thresholds increase with family size to accommodate higher living costs.

Using the underwriting charts below, match your region and family size to find the minimum residual income needed to qualify for a VA loan.

Understanding how to read and use these charts is crucial for prospective VA loan applicants.

They provide clear benchmarks to strive for in financial planning, ensuring that veterans and active military members are well-prepared to meet the VA’s unique lending criteria.

Submit Your Loan ScenarioThe VA sets specific residual income guidelines that vary by region across the United States, recognizing the general cost of living differences that come with different areas.

For example, the required residual income for a family of four in the Northeast is different from that in the South or Midwest.

Additionally, the larger the family size, the higher the residual income needed to qualify for a VA loan.

This approach was designed to ensure that veterans and military families have enough financial cushion each month to comfortably handle life’s unpredictable circumstances.

Meeting or exceeding the VA’s residual income requirements may seem daunting, but there are strategies to help.

To increase monthly residual income, veterans and military members might consider:

Another strategy could be exploring additional income sources, whether through part-time employment, freelancing, or investments—each or a combination could also contribute significantly.

In some cases, demonstrating strong financial health through other means may persuade lenders to proceed with the loan application.

A: Subtract your monthly debt payments, including your estimated new mortgage payment, from your net monthly income. The remainder is your residual income.

A: The calculation considers debts such as credit cards, loans, and your future mortgage payments. It does not deduct typical living expenses like utilities and groceries, as the residual income is intended to cover these.

Understanding and adhering to the VA loan residual income requirements are fundamental steps in securing a VA loan.

These requirements should not be looked upon as hurdles.

Instead, they are designed to be safeguards, ensuring veterans can comfortably afford homeownership without overextending themselves financially.

By preparing and strategizing to meet these standards, veterans and military members position themselves for better chances of success in the homebuying journey.

Are you a veteran or active military member considering a VA loan but unsure about the residual income requirements?

Learn about your mortgage options by completing our simple form.

We can connect you with the top VA loan lenders in your area to begin your homebuying journey.

Our advice is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.