Get Expert Financing

- Matched with investor-friendly lenders

- Fast pre-approvals-no W2s required

- Financing options fro rentals, BRRRR, STRs

- Scale your portfolio with confidence

VA assumable loans offer a unique opportunity in the mortgage market, but many homebuyers and sellers are unfamiliar with how they work. At My Perfect Mortgage, we often field questions about this special type of loan transfer.

Understanding how VA assumable loans work can open doors for both buyers looking to secure favorable terms and sellers aiming to make their properties more attractive. Let’s explore the ins and outs of these loans and their potential benefits.

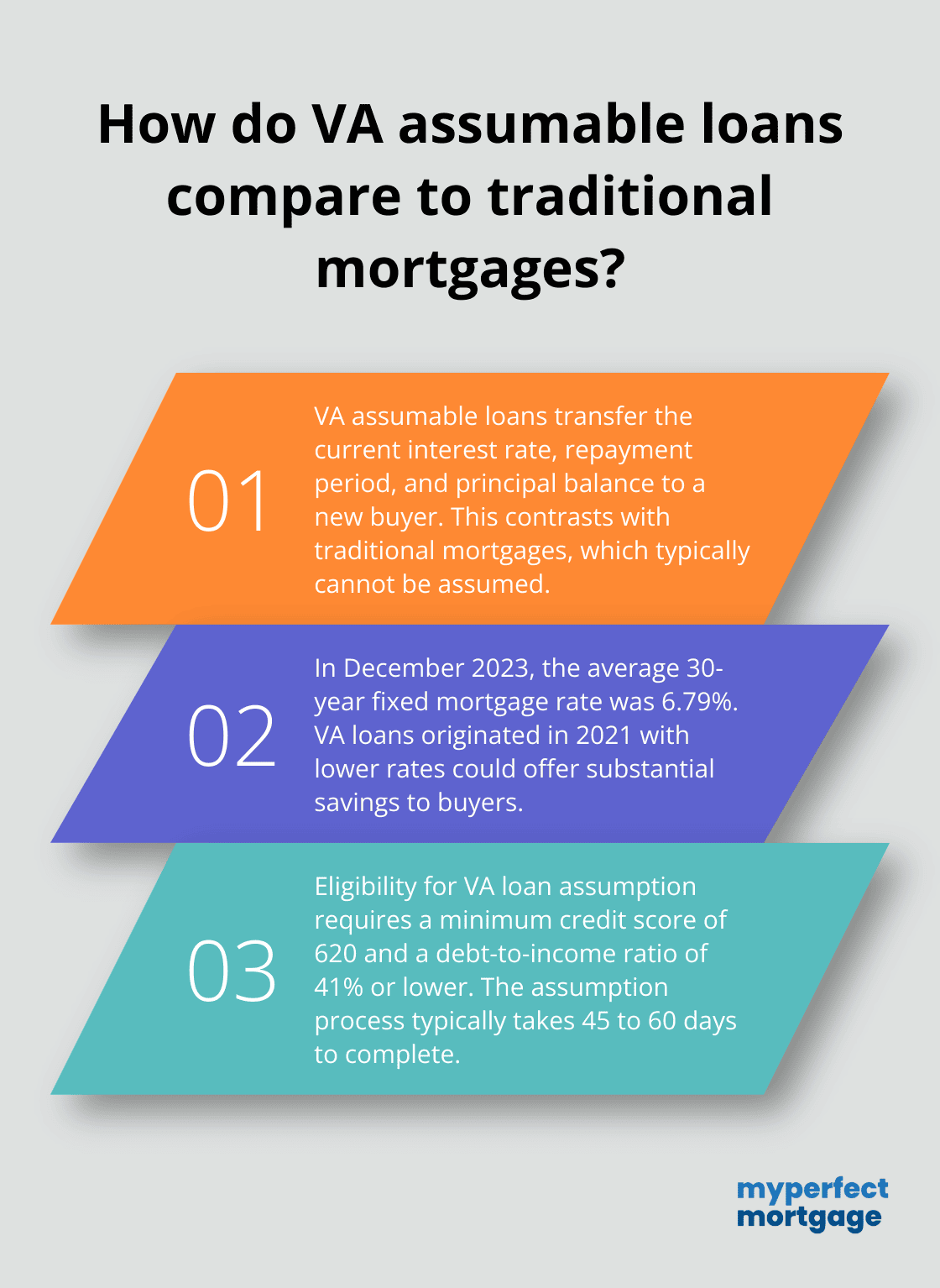

VA assumable loans allow qualified buyers to take over the existing mortgage of a VA loan holder. This unique feature transfers the current interest rate, repayment period, and principal balance to the new buyer. The assumability of VA loans sets them apart from most conventional mortgages, offering potential advantages in a rising interest rate environment.

The assumability of VA loans contrasts sharply with traditional mortgages. For instance, if current market rates hover around 7%, but a VA loan originated in 2021 has a 3% rate, the savings for a buyer could be substantial. The Mortgage Bankers Association reported an average 30-year fixed mortgage rate of 6.79% as of December 2023. Historical mortgage rates fell to historic lows in 2020 and 2021 during the Covid pandemic.

While VA loans typically serve veterans, active-duty service members, and eligible spouses, the assumption process opens these loans to a broader pool of buyers. However, strict eligibility criteria apply:

(These requirements may vary by lender.)

Assuming a VA loan involves several steps:

The timeline for this process typically ranges from 45 to 60 days, depending on lender and transaction complexity.

Locating properties with assumable loans requires some effort. Real estate agents experienced in military relocations often prove helpful in this search. Additionally, online platforms and multiple listing services (MLS) sometimes indicate whether a property has an assumable loan. (Buyers should verify this information directly with the seller and lender.)

As we move forward, let’s explore the significant benefits that VA assumable loans offer to both buyers and sellers in today’s dynamic real estate market.

VA assumable loans offer significant advantages in today’s real estate market. These benefits extend to both buyers and sellers, making them an attractive option in various economic conditions.

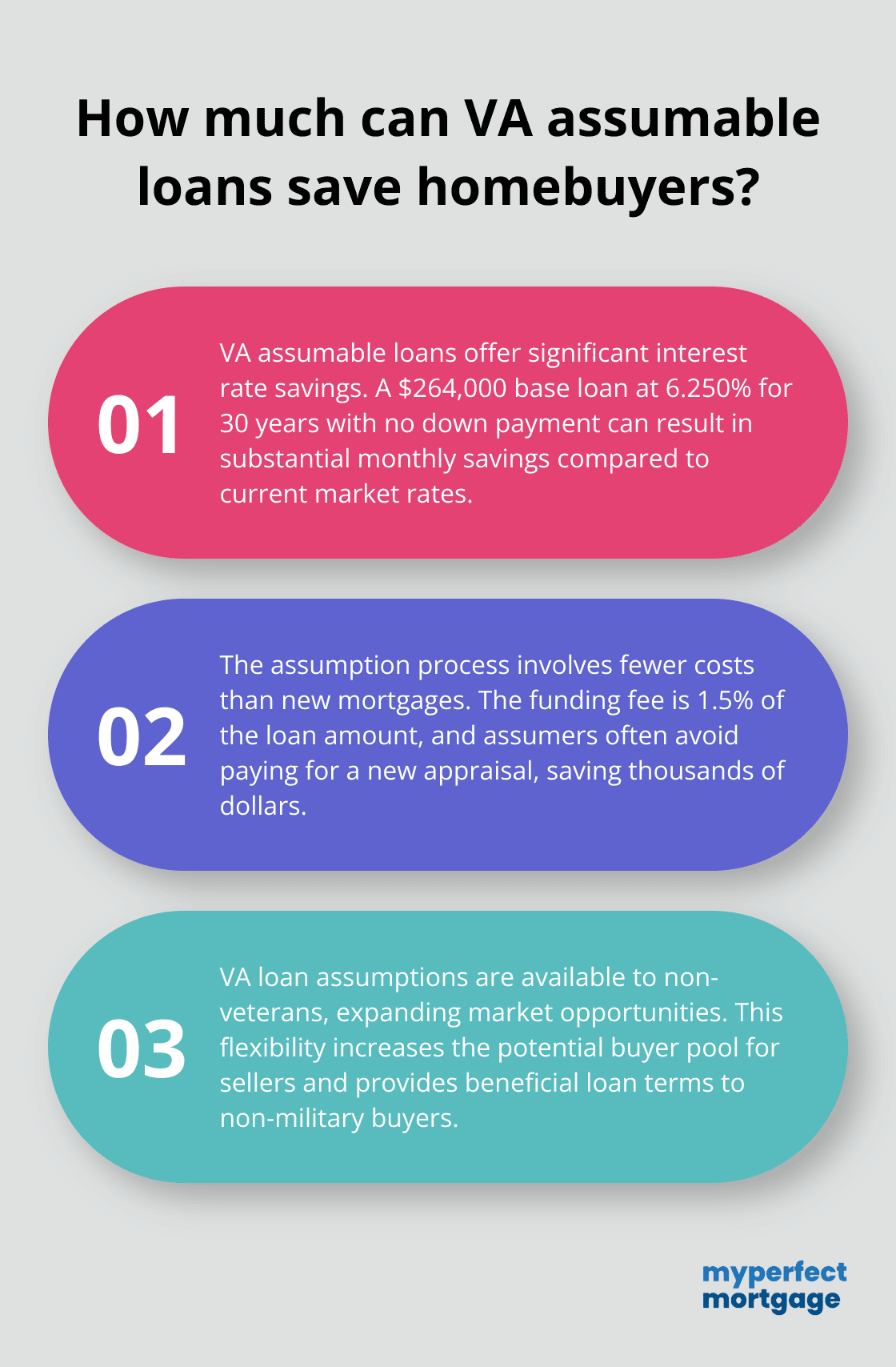

In a rising rate environment, VA assumable loans can lead to substantial savings. For instance, a $264,000 base loan amount with a 30-year term at an interest rate of 6.250% with no down payment could result in significant monthly savings compared to current market rates. This difference highlights the potential for significant long-term savings through loan assumption.

The assumption process typically involves fewer costs than originating a new mortgage. The funding fee for assuming a VA loan is 1.5% of the loan amount, not the purchase price. Additionally, assumers often avoid paying for a new appraisal, further reducing out-of-pocket expenses. These savings can amount to thousands of dollars, making home purchases more accessible for many buyers.

Sellers with assumable VA loans have a unique selling point in a competitive market. When interest rates are high, the ability to offer a lower rate through assumption can attract more potential buyers. This advantage can lead to faster sales and potentially higher sale prices. Real estate agents experienced in military relocations often highlight this feature in listings, expanding the pool of interested buyers beyond just veterans and active-duty service members.

The VA loan assumption process is often more straightforward than applying for a new mortgage. Buyers need to meet specific credit and income requirements, but they can avoid some of the more complex steps associated with new loan origination. This streamlined approach can save time and reduce stress for both buyers and sellers.

One often overlooked benefit of VA assumable loans is their availability to non-veterans. VA loan assumption requirements don’t necessarily restrict the buyer to being a veteran. This flexibility increases the potential market for sellers and provides opportunities for non-military buyers to access these beneficial loan terms.

As interest rates fluctuate and the real estate market evolves, VA assumable loans continue to offer unique advantages. The next section will explore the specific steps involved in the VA loan assumption process, providing a clear roadmap for those considering this option.

The VA loan assumption process starts with locating a property that has an assumable VA loan. This task can present challenges, as not all VA loans allow assumptions, and those that do aren’t always clearly advertised. Real estate agents with VA loan expertise can provide valuable assistance. These professionals often maintain connections within military communities and can access listings that specifically highlight assumable loans.

Online resources also offer help in this search. Some multiple listing services (MLS) include search options for assumable loans (though this feature isn’t available everywhere). Websites that focus on military home sales sometimes prominently feature properties with assumable VA loans.

After identifying a property with an assumable VA loan, the next step involves contacting the current lender. The lender’s approval is essential for the assumption to proceed. They will provide an application package that typically includes:

The lender will conduct a credit check as part of this process. Most lenders require a minimum credit score of 620 for VA loan assumptions (though some may set higher thresholds).

The underwriting process for a VA loan assumption mirrors that of a new mortgage. Lenders review the applicant’s financial situation to ensure payment affordability. This review includes calculating the debt-to-income ratio, which typically needs to stay at or below 41%.

During this stage, the Department of Veterans Affairs verifies the loan’s eligibility for assumption. They check that the current borrower has maintained up-to-date payments and that the loan meets current VA guidelines.

Upon approval, the process moves to the closing stage. This step involves signing legal documents that transfer both the loan and property ownership. Buyers must also pay the VA funding fee, which is typically 0.5% of the loan amount for assumption. (Some buyers, such as those receiving VA disability compensation, may qualify for exemption from this fee.)

The VA loan assumption process typically takes 90-120 days to complete, though complex cases may require more time. Common obstacles include:

Close communication with the lender throughout the process is key. Quick responses to requests for additional information can help keep the process moving smoothly.

VA assumable loans offer a unique opportunity in today’s mortgage landscape. These loans allow qualified buyers to take over existing VA mortgages, potentially securing lower interest rates and reducing closing costs. The process of how VA assumable loans work involves finding an eligible property, meeting credit and income requirements, and navigating the lender’s approval process.

VA assumable loans can lead to significant savings for buyers, especially in a rising interest rate environment. Sellers with assumable VA loans have a powerful marketing tool, which can attract a wider pool of potential buyers (potentially leading to faster sales and better offers). Both buyers and sellers should carefully consider the implications of a VA loan assumption, including financial qualifications and effects on VA loan entitlement.

At My Perfect Mortgage, we specialize in guiding clients through various mortgage options, including VA assumable loans. Our platform matches you with lenders experienced in VA loan assumptions and provides tools and resources for informed decisions. We can help you navigate the VA assumable loan process with confidence, whether you’re a buyer or seller.

Our advice is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.